Last month, Philippines was included in top 20 of world’s economy in terms of GDP growth prediction for 2015. Next to China which is number 1, we are number 2! So what does it mean to us?

The good news is that this is another great opportunity to gain more profits this year through the stock market. If you are already an investor, congratulations! If not, then its time to take action and to be one.

With the help of the internet technology, investing is now made virtually available to all so it’s merely an open mind, a decision and a courage to take the necessary to steps on becoming an investor.

Many people specially in social networking media like Facebook raised their eyebrows when this good news just popup despite the Mamasapano issues where we are immersed for several weeks or even more than a month now.

Some people can’t believe and expressed their views like “This is amazing but how come I see lots and lots of poor people on the street?” and “so what’s in it for me then”. In short, many Filipinos still don’t realize how to take advantage of this good news.

Let’s proceed and highlight what’s the deal with this good news for our beloved country.

Based on COL report, this year 2015 will boost government’s “legacy spending” and normally happens before the change of administration takes place which will be next year. This will mean more jobs and more projects that will benefit giant companies to name a few like Ayala Corporation, SM Prime Holdings, and other industries like banking and consumers.

Low oil prices. Last January, the price of oil started to drop. Although it went up after several weeks, it is still low compared from the past. The money we save on gas will also increase consumer spending which local companies and businesses will then again benefit from these.

Philippines is also on top of BPO industry. This means apart from the huge amount of remittances of OFWs, there’s also bulk of money circling around that will trigger spending in consumer and other businesses like real estate and banking. More people will spend money to buy condos, cars, gadgets, travel, etc. and the list goes on and on.

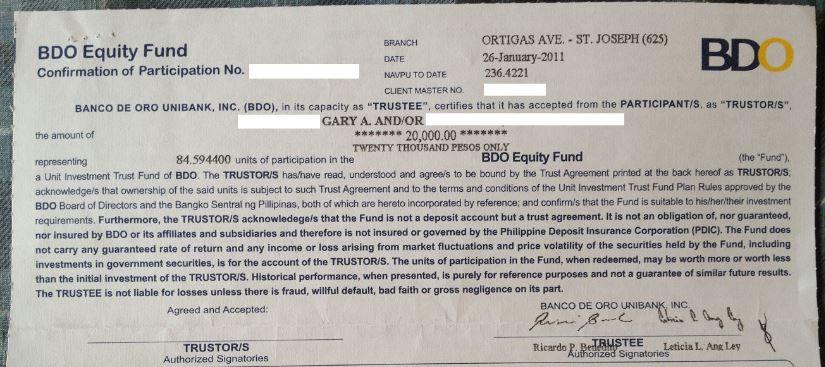

The key to profit in this good economy is to participate and “ride” this great companies in its growth by buying its shares in the stock market. The more earnings they will have means more profit for us the investors.

Now the question is, are you an investor? If you are, then once again congratulations! Because this year will be a great year for us all.

If you are still planning to invest and want to jump in right away, I invite you to join Bo Sanchez’ Truly Rich Club for guidance in the stock market. To join click here.

“If you think education is expensive, try ignorance” — Derek Bok